Why Backtesting Is the Foundation of Every Successful Trader

The difference between having a trading idea and having a successful trading strategy is huge. It is possible to look at price charts for many hours, to find one pattern that appears to be ideal, and then become very confident in that trade. However, being confident does not guarantee that a profit will result. Backtesting will enable us to know if our trading strategy would have been profitable or not if we had actually executed trades using that strategy.

The knowledge of backtesting before execution is something all professionals do; they do not take that chance because it may be very costly. If you manage an investor's money or have large amounts of money in your fund, you need to know that whatever method you are using to make trades has been proven through a variety of test cases over time, not just a few good trades in the recent past. Many firms, including Bridgewater and other large hedge funds, validate their method over years by going back-testing before they risk one dollar trading in real time.

Many traders fail to understand the importance of backtesting their trading strategies. Backtesting allows you to see how your strategy would have performed in different market conditions and over different time periods. This provides you with valuable information to help you better understand your own feelings about risk and to develop your own successful trading strategy.

Many traders think that if they have a good strategy on paper, it will be successful. However, this is often not the case. Many factors can cause your strategy to fail during a market crash, a sudden spike in volatility, or when market conditions change completely. The only way to know how your strategy will perform during these conditions is to backtest your strategy. Otherwise, you will be trading blindly and not know the maximum drawdown, the win rate, or what your maximum loss tolerance is.

Think of it this way. You can use a textbook as a guide to prepare for an exam. If you score well on ten years of past exams using the same study method, you can see how reliable your study method is across many different examination formats and difficulty levels. While you can't guarantee that you will pass the real exam, you have plenty of evidence that you can use to determine your success on future exams.

The data-driven approach you get from backtesting will also help you avoid the traps of emotional trading. When you see that your backtested strategy has a 40% win rate and a 3:1 reward-to-risk ratio, you can continue to trade your strategy even when you experience a losing streak. Instead of letting your emotions drive your trading decisions, you are trading based on the evidence you have collected. This objective mindset separates the profitable trader from the trader who quits after three bad weeks.

Core Concepts Every Trader Must Know Before Backtesting

To conduct a backtest effectively, you must begin with a thorough understanding of what constitutes a successful backtest. This knowledge will help prevent you from falling into common pitfalls that produce unreliable results.

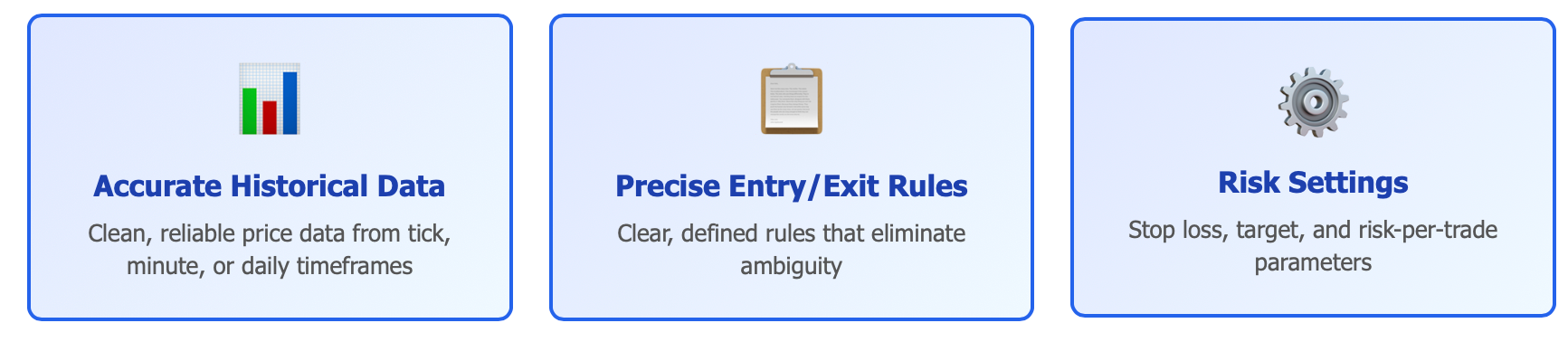

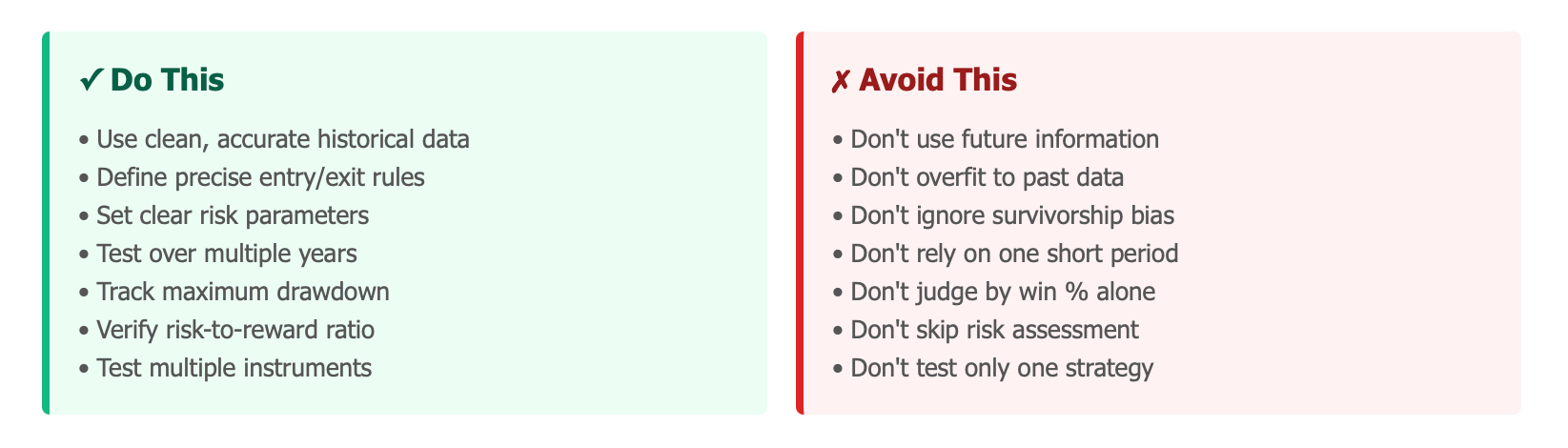

Every successful backtest has at least three key components: accurate historical price data, precise rules for entering and exiting trades, and risk settings. Simply importing price data and hoping it produces positive results will not yield success. The historical data used for analysis must be clean and accurate. Regardless of whether you choose to analyse tick data, 1-minute bars, or daily candles, the quality of your historical data will determine the quality of your backtest results.

Your entry and exit strategies must be so precise that another trader would reach the same decision as you based on the same information. For example, saying "When the price looks good, buy" is vague and not helpful. You should clearly define the rule as something along the lines of "When the 50-period moving average crosses above the 200-period moving average on a 4-hour chart, buy". Similarly, your risk parameters are equally important. How much are you willing to risk per trade? Where is your stop loss positioned? What is your target? These parameters should be incorporated into the development of the backtest strategy from the outset.

Here's where you need to pay a lot of attention – understanding the things that could lead to backtesting mistakes.

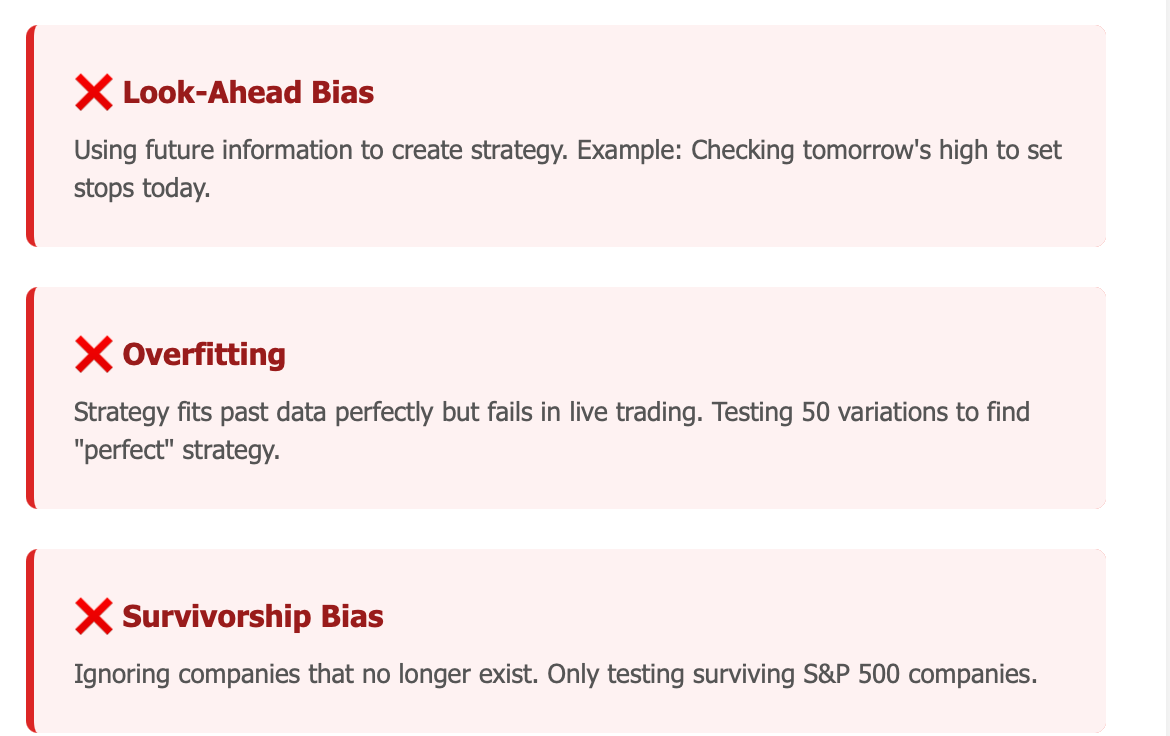

One of the big problems with backtesting is look-ahead bias. This happens when you accidentally use future information to create your strategy. An example of look-ahead bias is when you check tomorrow's high to set your stops today. Your backtester will give you fantastic results, but you will never see tomorrow's high live while you are trading and will therefore lose money on your live trades.

Another problem for traders is overfitting. Overfitting can occur when you have a strategy that can be made to fit the historical data you have; however, you are just learning random patterns and not developing a strategy that has repeatable results. For example, if you have a strategy that has a 95% win rate, because you tested 50 different strategies, you could say you found a 'perfect' strategy for past data. Your strategy will never earn you a single penny once it is no longer 'perfect.'

Lastly, the survivorship bias that many traders fall into is a big mistake. When you backtest the S&P 500, you backtest companies that are still listed there today, but there were thousands of companies on the S&P 500 over the last 20 years that no longer exist. Therefore, there is a lot of losses that are ignored, and your backtest presents a much brighter outlook than reality.

Backtesting should not create a 100% foolproof system, but rather a realistic system that you can believe in when the going gets tough.

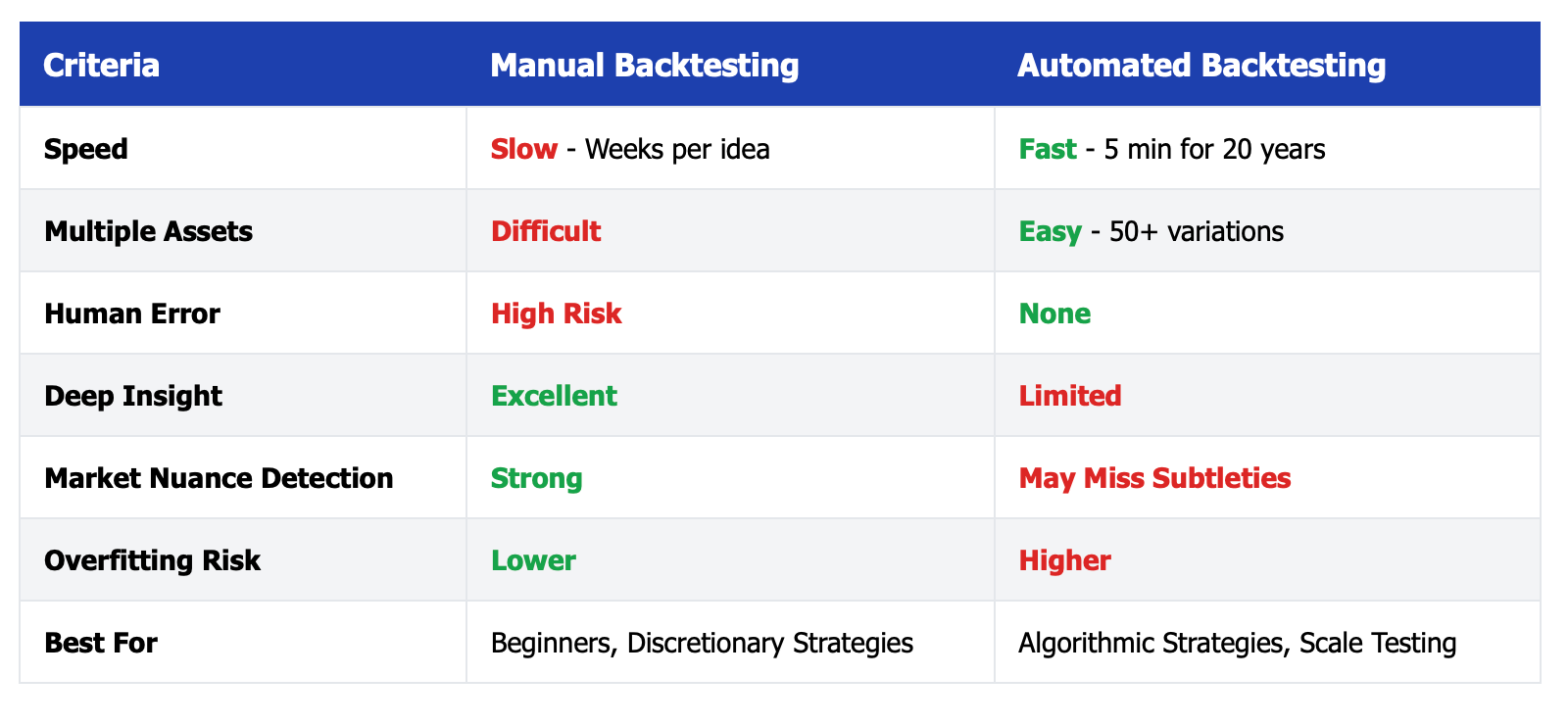

Manual Backtesting: A Beginner-Friendly Yet Powerful Method

Walking back through historical charts, looking for your trading signals, and recording your trades is manual backtesting. It's painstakingly slow, but it is one of the highest quality methods for fully understanding your strategy.

Manual backtesting works exceptionally well for beginner traders and those who are using discretionary pattern-based trading strategies. Manual backtesting requires the trader to become fully immersed in the marketplace in a way that cannot be matched by any automated tools. Through manual backtesting, the trader can see how the price moved leading up to their trading signal; what occurred after they entered their trade; and why one trade was profitable while another trade was unprofitable.

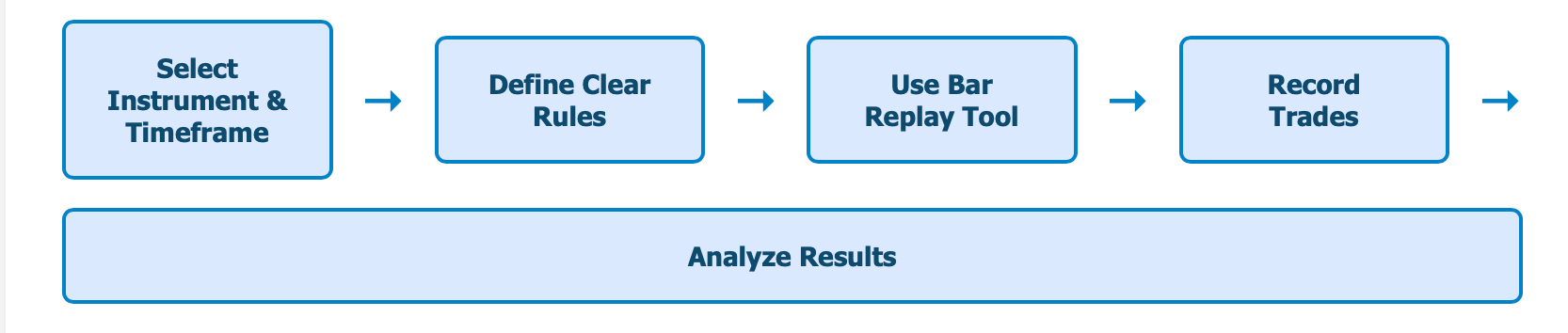

To perform this process correctly, you will want to first select the instrument that you will be trading, along with the timeframe of your trades. For example, let's say you were going to be trading EUR/USD, and you would be trading on a 4-hour interval. You will also want to define your rules for your strategy as clearly as possible (write them down). An example of a rule would be "I enter long when price breaks above the highest price in the last 20 days, and also the 50-period moving average is sloping up".

Next, you will want to use a method like TradingView's bar replay feature to go through your charts day by day and take note of your trades when you meet your entry criteria. As you take notes, include the Date (when the trade happened), the price (where you bought), and either the Exit Price (where you sold) or the amount of profit or loss that you had on the trade. Continue to do this until you have gone through the data for many months, if not years.

At the end of this process, you will now have a record of all your trades that you made, along with the amount of winning and losing trades, the average winning and losing trade amounts, as well as the longest losing streak you had. This information represents the actual data that describes how your strategy was performing during that period.

If a trader were to test, for example, a trend-following strategy over a period of ten years of EUR/USD historical data, that trader would be able to determine how the strategy returns 12% annually with a maximum drawdown of 8%. These numbers are not just numbers on a spreadsheet; they are a result of the trader manually reviewing thousands of different price bars to see (and to understand how) and when the strategy worked during that time period.

Manual backtesting requires time, effort, and consistent application of a formula when a condition meets the criteria.

The major disadvantage of backtesting manually is speed. Although you can backtest one asset over multiple years in a reasonable time frame, you may not have the ability to backtest multiple strategies or compare performance across several different assets. You would then look to utilise automated backtesting options.

Automated Backtesting: The Professional Approach for Speed and Scale

Automated backtesting allows you to run a strategy across multiple data sets simultaneously. You create the strategy in a programming language or by using a visual builder provided by some platforms, provide it with historical price data, and let the system calculate your results. There is no need for you to click charts manually or to record trades by hand.

For example, if you are a quantitative trader testing a strategy against an extensive historical price history of gold using different volatility levels and testing that same strategy against 15 different currency pairs at the same time, it will take months to perform the testing. Using automated backtesting, however, allows you to conduct these same tests in just hours with the use of a computer program instead of a human.

The importance of automated backtesting lies in the fact that it does not allow for human intervention when applying trade rules and executing trades. A computer executes a strategy exactly as provided, without hesitation or overconfidence related to losing trades or winning trades. The consistencies in this manner of using automated backtesting provide you with results that are trustworthy.

You simply select a Backtesting Application from the list of available Backtesting Applications (MetaTrader 5, cTrader, NinjaTrader, and Backtrader) and enter your Rules for the Strategy either by selecting buttons or composing the Code. Then you select the Time Period and Asset to backtest against. Afterwards, you click Next or Run/Start, and in seconds you'll receive an Equity Curve, Drawdown Chart, and Risk/Reward Metrics (Sharpe Ratio, Maximum Drawdown, Profit Factor, etc.).

The power of Automated Backtesting comes from its ability to perform Automated Backtests for all types of Market Conditions and Time Periods using multiple Instruments. It also allows for Sensitivity Analysis for the Strategy you are Backtesting to evaluate how changing the Input Parameters slightly affects the Strategy's Performance. Finally, you can backtest a New Strategy as easily as Brewing Coffee.

For example, when you conduct an Automated Backtest of a 5-year Simple Moving Average Crossover Strategy using Gold, the results of that Automated Backtest may show that the Strategy has produced an Average Annual Return of 8% with a Maximum Drawdown of 22% in 2020. You now have a clear understanding of what you can expect from this Strategy and can determine if you wish to continue trading with it or not.

How to Evaluate Whether a Backtest Is Truly Reliable

There are many ways to assess a strategy in backtesting, and while two traders may use the same strategy for backtesting, they will receive totally different results due to the amount of data, the parameters used in the strategy, or mistakes made while backtesting the strategy. The ability to evaluate backtests is extremely important.

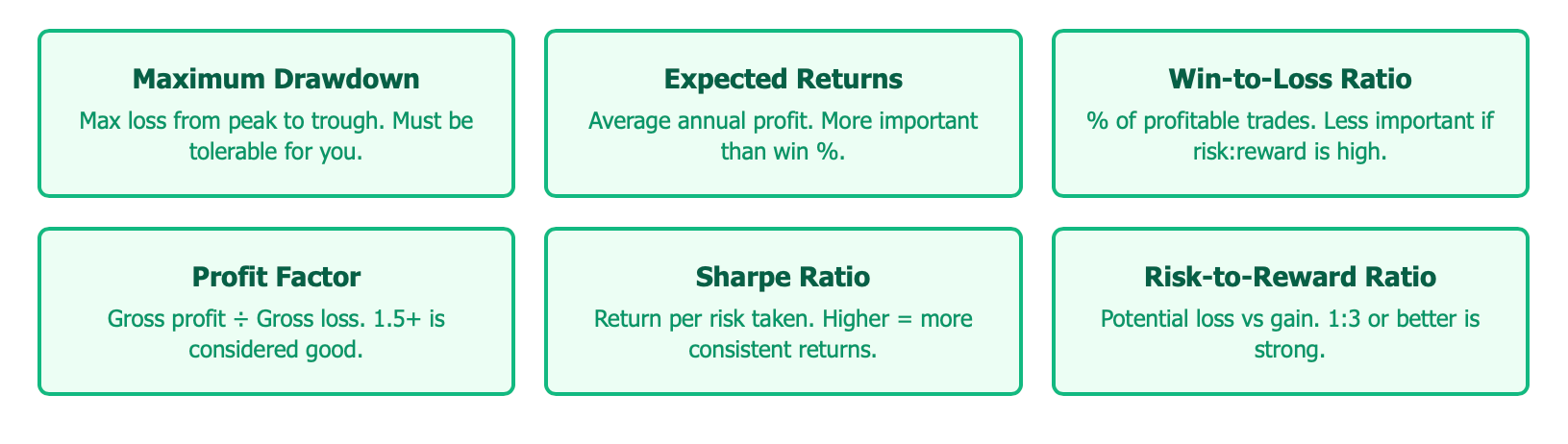

You should always refer to the two primary key performance metrics to determine the reliability of the backtest. The maximum drawdown is an indicator of the maximum amount of money that was lost during the optimised backtest. A strategy can be up 30% and then be down 40% at some point in the backtest; this should be considered before taking the trade when determining if you can endure that amount of loss before selling an investment in panic.

Expected returns refer to how much profit the strategy will produce each year on average. The win-to-loss ratio refers to the percentage of trades that were profitable. The main reason for this comparison is that an extremely high win percentage does not have any value in assessing the true strength of a trading strategy unless the strategy has a very attractive risk-to-reward profile.

Thus, for example, the profits from a trade with a win percentage of 30% and a risk-reward ratio of 1:5 can far outweigh the losses from a trade with a win percentage of 80% and a risk-reward ratio of 1:0.5, since trades that lose a lot will likely not have as much impact as trades that win a lot.

The profit factor is defined as the total gross profit (the total money earned through profit) divided by the total gross loss (the total money lost due to loss). A profit factor of 2.0 means that for every $1 lost, the trader will receive $2 in profit. Generally, anything above a profit factor of 1.5 is considered a good profit factor.

The Sharpe ratio gives traders an idea of the return they get for the risk taken. If the Sharpe ratio is high, it indicates that the trader is generating steady returns. In other words, a high Sharpe ratio indicates that a trader's returns are more predictable and less influenced by chance. A trader's strategy that produces 20% returns but is highly volatile could have a lower Sharpe ratio than a strategy that returns 15% consistently.

When evaluating a backtest, do not evaluate solely on profitability. Evaluating the risk and volatility of a strategy is critical. A strategy that returns 15% profits with an 8% maximum drawdown is much easier to trade than a strategy that returns 30% profits with a 50% maximum drawdown. Ultimately, you should be able to sleep well at night.

Manual vs Automated Backtesting: Which One Should You Use?

You don’t have to decide between these two approaches; most traders will use both over the course of their development. Manual Backtesting provides a higher level of insight. You will gain a greater understanding of each trade, the surrounding context, discover patterns that may not show up through an automated test, and use that knowledge to develop a gut feeling about when your strategy works best.

This means Manual Backtesting is a perfect tool for developing discretionary strategies or for new traders who are learning about Backtesting and want to develop a solid foundation before using Automated Backtesting.

With Manual Backtesting, you trade off certain advantages. First, it can take time to build sufficient speed for many trades; therefore, it’s not an easy way to build an automated trading system across several assets. Secondly, because the trader is limited in their ability to track and collect data from multiple pairs, there is a risk that the trader could miss important pieces of data or introduce errors during recording. In general, a trader can expect to execute an idea every several weeks using Manual Backtesting versus the speed of Automated Backtesting.

Automated Backtesting is a speed demon. You can run 20 years’ worth of data through your algorithm in less than five minutes. You can also run 50 different variations of your algorithm simultaneously. You can use the results to validate your approach and apply it across as many as ten currency pairs at the same time. Finally, it eliminates human error in executing trades. This cannot be underestimated when using algorithmic or high-frequency trading techniques.

One disadvantage of Automated Backtesting is that by following predetermined rules, the system may miss subtle changes in market conditions that a skilled discretionary trader would be able to identify. Additionally, the ability to continually change parameters could lead to overfitting to the maxim, and thus no longer prove to be a valid or statistically sound strategy in future performance.

Traders often take a manual approach to develop their trading strategy's foundation, then implement this strategy for the small size of live trading so they can track performance, then transfer that experience into automation for longer time periods using more diverse instruments as a way of verifying that their strategy is robust from both short and long-term testing.

For example, manual testing allows a trader to confirm that a strategy will perform well using real market conditions. With automated testing, a trader can see how the same strategy operates over longer time frames and in different trading structures.

The decision on how to proceed depends on the type of trader you are, how complicated the strategy is, and how much data you need to validate your strategy. For instance, if you rely solely on simple patterns to trade, you may find that testing them through manual means will work well for you. If you build out your strategy via complex algorithmic approaches, you'd be wise to automate that process. Most traders would do best by starting testing manually and then transitioning to automating as they grow.

Conclusion: From Backtest to Live Trading

You can't rely on backtesting to predict how you will perform. While backtesting can't predict how successful your trading strategy will be, backtesting will show you honestly that your plan has validity to work. In turn, backtesting can help build your confidence to stay in long enough during your losing periods while waiting for your strategy to revert to a profitable state.

People who have had success trading long-term typically do so due to their disciplined approach rather than their high-risk strategies and large trades. Successful traders do this by systematically performing testing on their trading ideas, assessing the risks of their strategies, and acting methodically in executing their plans. Backtesting will assist traders with developing their edge in the marketplace.

If you have never done any backtesting before, I recommend that you begin performing manual testing. Review the charts to locate the signals that you would have used and the profits (or losses) that you would have incurred. After you have gained enough experience with manual backtesting, you can implement auto engines to backtest your strategies to a larger extent. Once you have become familiar with both manual and automated backtesting methodologies, you will have developed profitable strategies through thorough testing.

Call to Action

At BTCDana, we help traders skip the learning curve with pre-tested strategies and backtesting tools built for real-world performance. Stop guessing whether your strategy works and start trading with confidence. Explore our backtesting platform today and join traders who've already stopped losing to emotion-driven trades.

Ready to transform your trading with data? Get started with BTCDana's strategy validation suite, where backtesting meets profitability.