Why Investors Lose Money in Long-Term Commodity Trading Even When Predicting Trends

You've done your due diligence by completing your technical analysis and analysing the supply and demand fundamentals on a global scale; you are now positive that the price of crude oil will continue to go up. Therefore, you purchased the commodity ETF and waited patiently for six months, only to find out that while the price of oil had increased by 15%, the value of your ETF was nearly at breakeven or had actually lost value from what you paid for it.

This is not a result of you making a trade or buying at the wrong time. Instead, you discovered one of the most significant issues that goes unaddressed with long-term commodity trading, which is that there is often a significant lag between spot price movements and actual return on investment.

What most investors fail to realise is that predicting market direction does not tell the entire story. Roll yield is a concept that describes how the internal structure of the futures market can affect returns positively and negatively. It is a force that affects returns in two ways: contango and backwardation.

This guide discusses three key areas that impact real returns on a long-term basis:

1. The true sources of commodity investment returns

2. How roll yield impacts your long-term positions in a commodity ETF

3. The effect of contango and backwardation on a commodity ETF's portfolio.

Consider it this way, knowing that oil is going up in value next year is similar to being aware that your salary will increase in value next year; however, if your supplemental cost of living increases at a rate greater than the increase in your salary, then you will still lose purchasing power, just as if you were ignoring market structure.

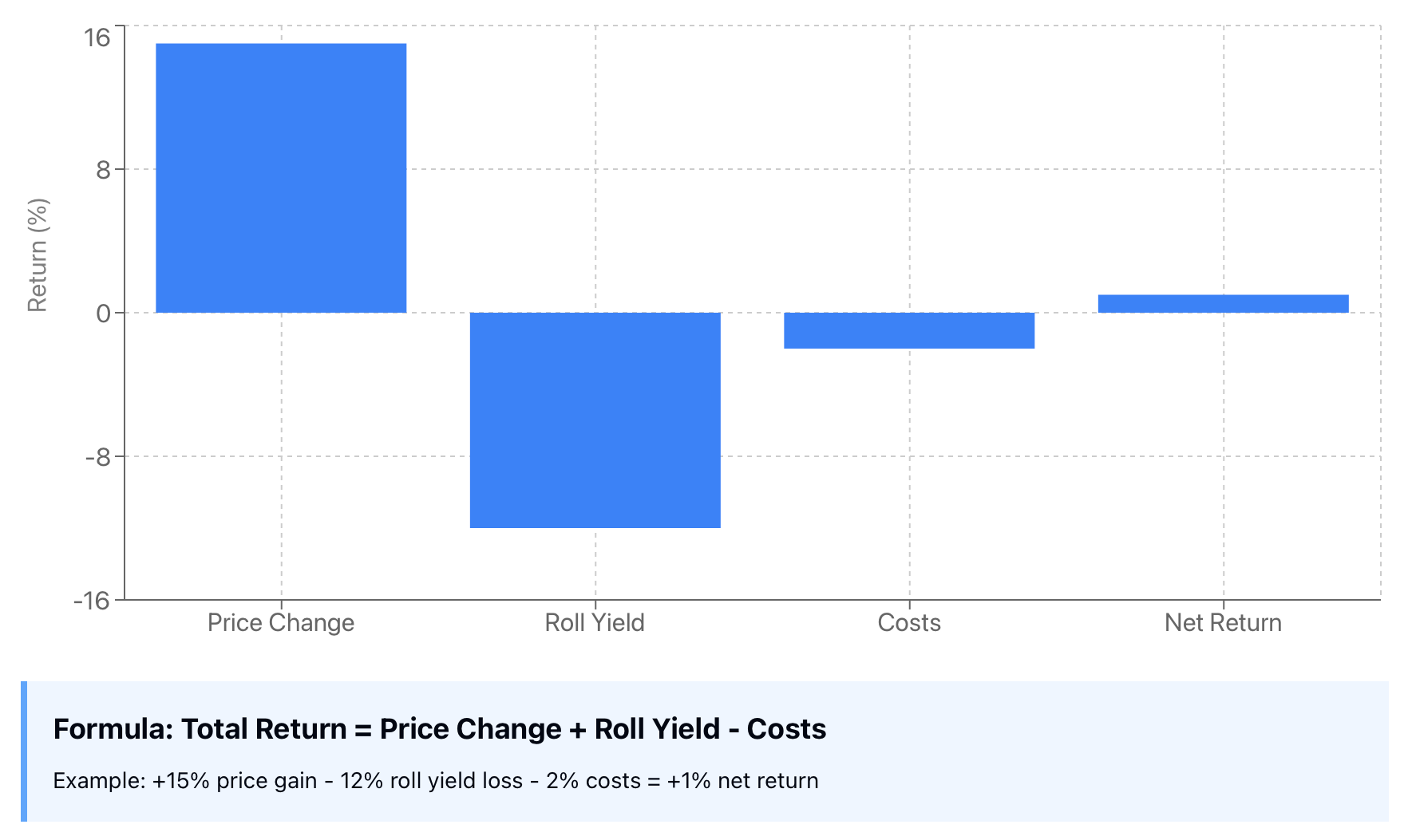

Main Point: Investment returns are based on both the direction of the price and what price will be, and how much the contract price will increase due to the contract roll costs.

Understanding Total Returns: Price Changes, Roll Yield, and Costs Explained

Investing in commodity ETFs or futures-based products comes with 3 major components that make up total return:

Total Return = Price Change + Roll Yield - Costs

Let's look at how this works through a basic example. If you buy a crate of apples every month to have for your business, and the price of apples goes up, you would earn revenue from those apples based on the price increase that you can sell the apples for. That discount is similar to a negative roll yield in a contango market.

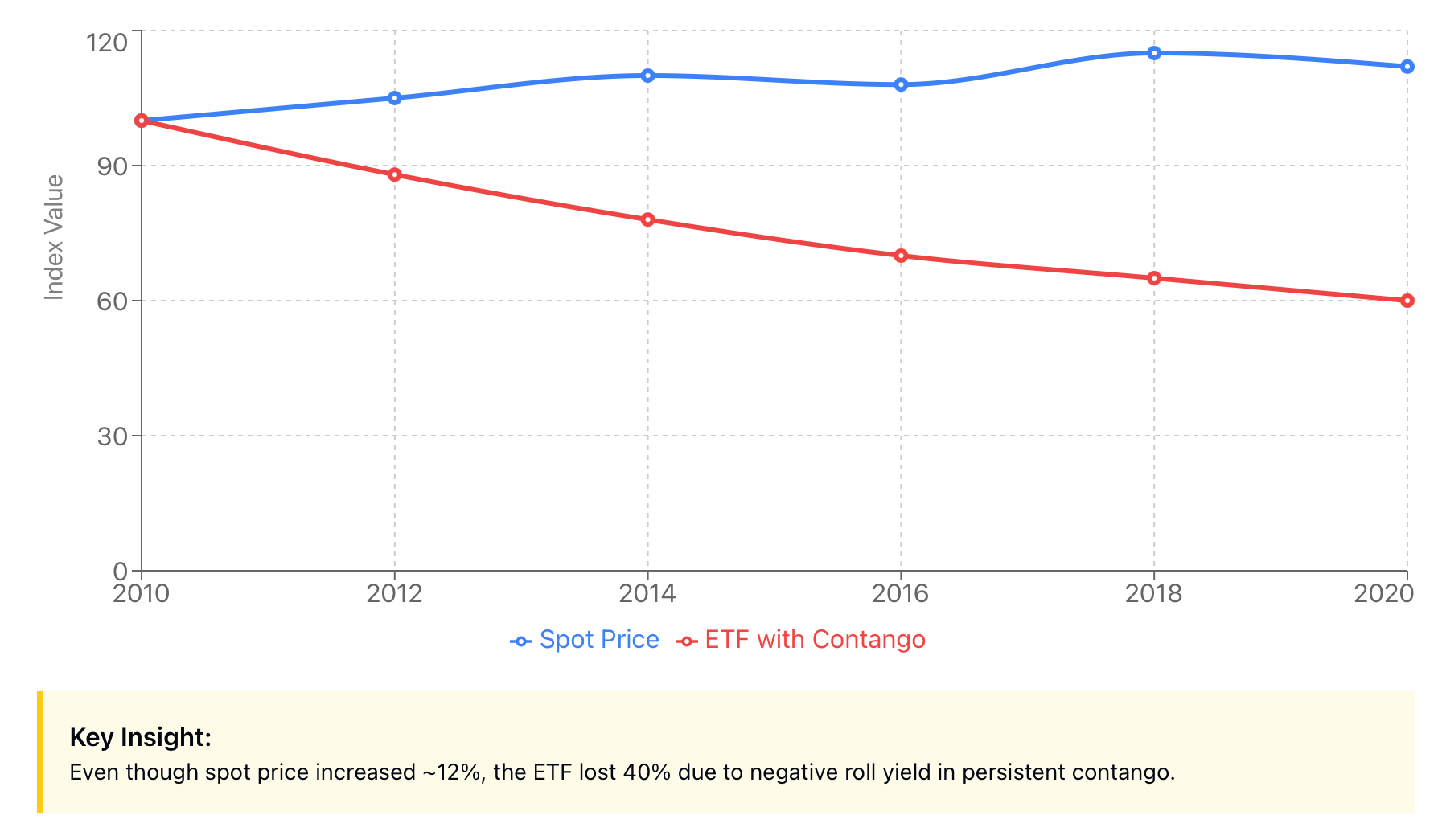

Now, let's take this through a real business example. The United States Oil Fund (USO) is one of the most popular energy ETFs. Between 2010-2020, the price of crude oil fluctuated, but USO consistently underperformed compared to the price of crude oil.

Why did this happen? Because USO has to "roll" its futures contracts every month. They sell the contracts they are holding that expire and buy new ones; however, the new ones are usually at a higher price because of contango. Therefore, USO's performance was continually being negatively impacted by roll yield, costing investors as much as 10-15% per year due solely to roll yield losses.

Here’s how the whole thing breaks down:

The three pieces are:

Price Change - What is shown on the charts, like the movement of the spot price

Roll Yield - Structural gain/loss associated with rolling over futures contracts.

Costs - trading costs, bid-ask spread, etc.

Roll yield can be just as big (if not bigger) than the price change for long-term profits/losses. In persistent contango markets, roll yield is the overwhelming factor determining profit or loss.

Summary: Roll yield is a structural gain/loss that affects long-term returns. It can often exceed the impact of movements in the actual commodity price.

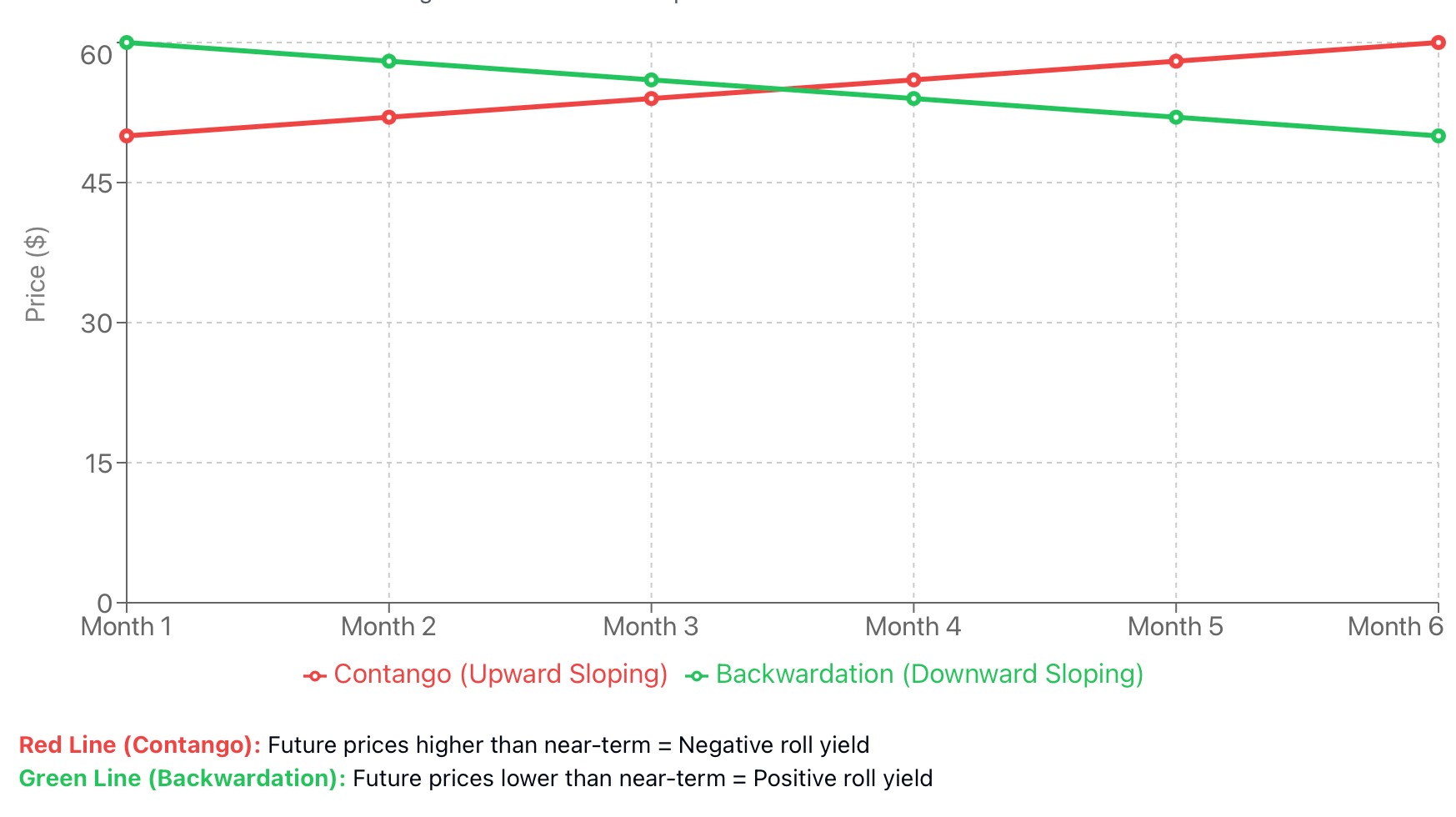

Contango vs Backwardation Explained for Traders and Investors

The concept of roll yield will require an understanding of both "contango" and "backwardation"; these are basic structures for the futures curve.

"Contango" occurs when distant futures prices are higher than near-month contracts; for example, say you're at a grocery store, and you want apples delivered next month: the price is $10 per crate. If those same apples are going to be delivered in six months, then the price is $15. Therefore, in contango, the market takes into account the cost of carrying and financing these commodities, as well as the cost of delaying consumption.

The opposite situation is backwardation: distant futures prices are lower than near-month contracts. For example, say you're looking for apples to be delivered next month: the price is $10 per crate, and for those same apples delivered in 6 months, the price is $8. Backwardation happens when there is immediate demand for that particular product or when there is a shortage of that product. There is a willingness to pay a premium to receive the product today versus delaying receipt until the future.

To put this into professional language, let's consider WTI crude oil. During the COVID-19 pandemic of 2020, the oil markets experienced severe contango due to filling up storage facilities and collapsing demand. For example, the May contract traded approximately $10 to 15 higher than the June contract. Because of this, whenever investors sold their near-month contracts to buy their next month's contract, they were forced to sell low and then buy their next contract for a higher price. Therefore, every month they rolled their positions, creating a large negative roll yield.

In contrast, oil markets will often be in a backwardated position during oil supply shocks or periods of heightened geopolitical uncertainty. Evidently, oil prices around December 2021 reflected that price increase in WTI at the front month, arising from pent-up demand from COVID-19. The WTI price at the front month was higher than future dates, resulting in long roll yields for those investors holding WTI positions for some amount of time.

The main things driving the above periods cause the following characteristics of oil markets:

-

Storage & Insurance Costs: Rates Put Pressure on Contango

-

Financing & Interest Rates: Rates Put Pressure on Contango

-

Supply Constraints or Extreme Demand: Put Pressure on Backwardation

-

Seasonal Variation: Patterns Connected to Agricultural Commodities

Takeaway: Understanding how these market structures operate in contango vs backwardation will help clarify your perspective toward investing or de-risking on your particular holdings over your timeframe.

Roll Yield Explained: How Contango and Backwardation Affect Your Investments

Investors usually don't know that roll yield exists, but it's the hidden force that can either supercharge or tank returns for your commodity ETF.

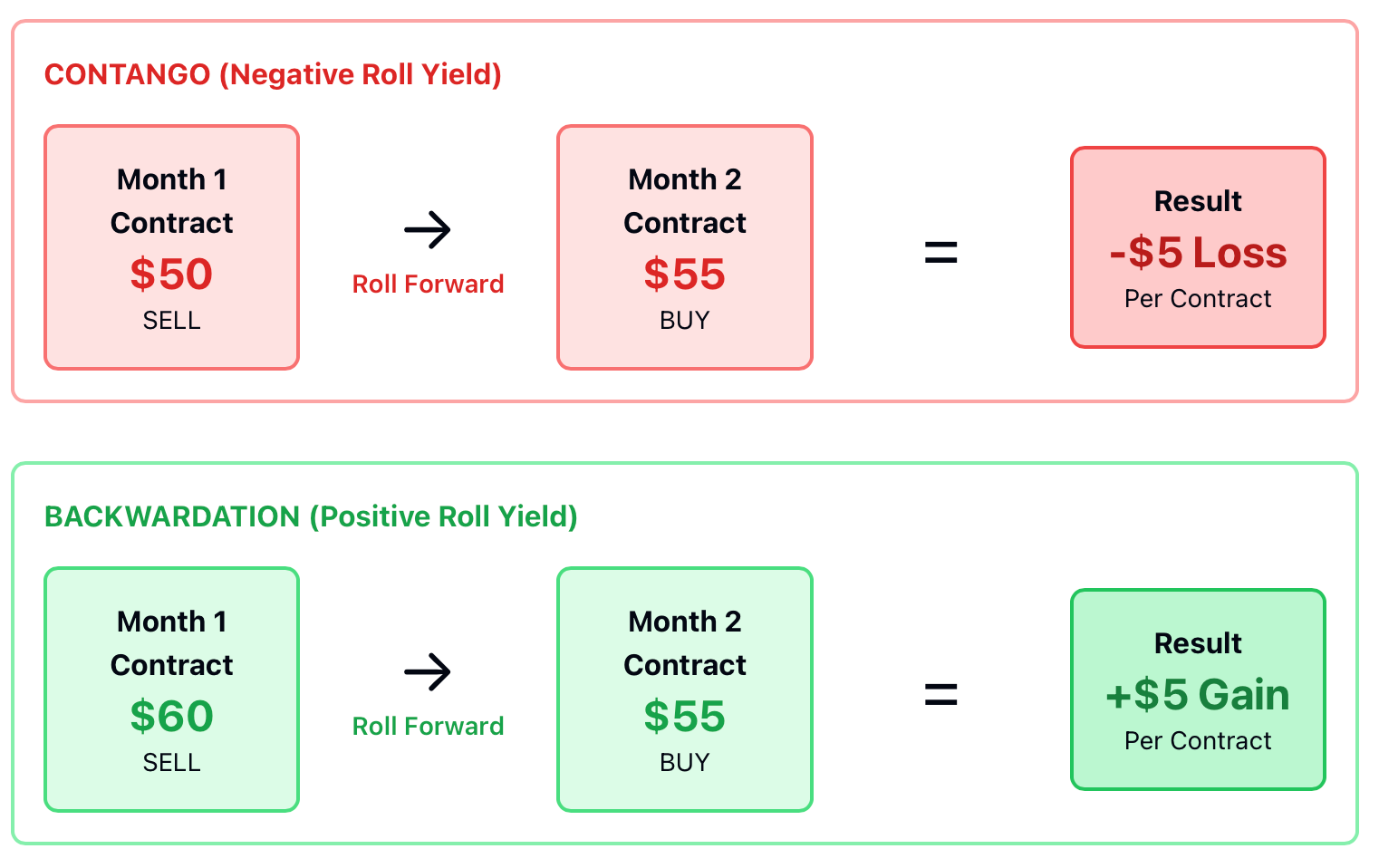

It works like this: futures contracts all have expiration dates. If you're currently invested in a commodity ETF or futures, you can't just maintain your position in the same contract indefinitely; you need to roll your position by selling the contract for the near month prior to expiration and purchasing the contract for a later month. This process creates the roll yield based on the price differential between the two contracts.

In a Contango Market, you will roll your position by selling at a lower price point and purchasing the next month's contract at a higher price point, resulting in a negative roll yield. So each month, you would lose a bit of value, simply due to the structure of the futures curve, and as time progresses, those losses would compound.

For example, in March 2020, USO was required to roll its April WTI crude contracts into May contracts. The April contract was trading at $20/barrel, while the May contract was trading at $26/barrel. By rolling contracts, you effectively sold the April contract for $20 and purchased the May contract for $26, resulting in an immediate 30% loss per contract, not considering any change in oil prices afterwards.

In Backwardation Markets, the opposite of Contango, where prices are higher now, and lower later, you can roll forward into higher prices and roll over into lower prices for a positive roll yield. Even though prices do not change from spot to future, you make structural profits off the curve's shape.

For example, during late 2007, when oil was in high demand, the near-month WTI contracts were trading $5-$10 higher than the later month contracts due to the need for immediate supply in refineries. Since then, every month that commodity investors rolled over their contracts, they would get the $5-$10 premium for rolling and earn an additional 5-10% on top of any price appreciation.

If you use the analogy of a crate of apples to illustrate the Backwardation Market for rolling, it works like this: You run a juice company and need fresh apples every month. If the apple prices were in contango (apples are getting more expensive), then you would pay more for the supply for next month than you did for this month when you sold your inventory. If the apple prices were in backwardation (apples are getting cheaper), then you would sell your inventory at a premium and buy back the supply at a discount for next month.

The key here is that roll yield is something you should expect to receive regardless of whether you have market timing skills or whether you were correct about the future price of the commodity; the roll yield is a result of the structure of the market. You may be absolutely correct in anticipating the direction of a commodity, but if the roll yield works against you, you will lose money.

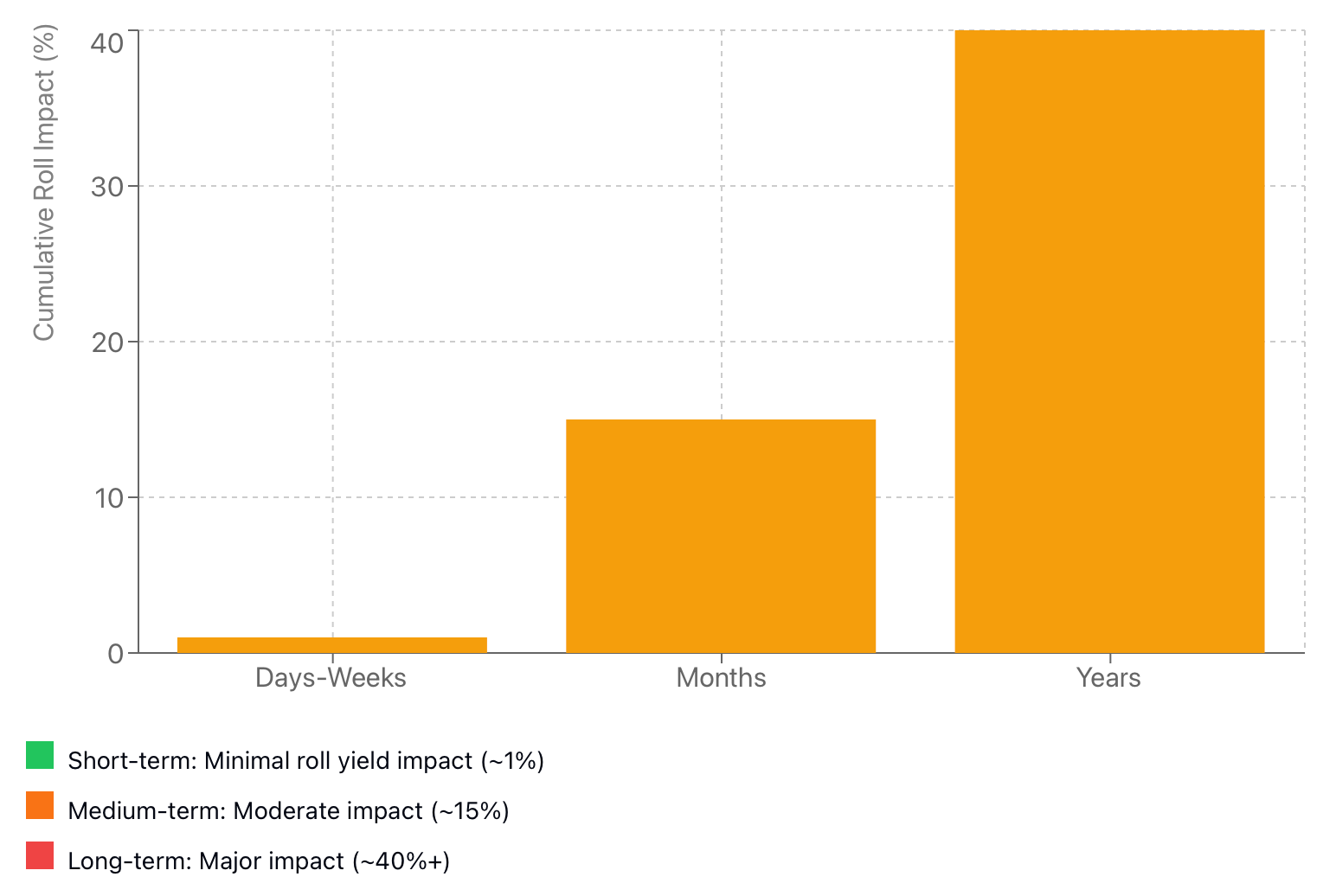

How Short-Term vs Long-Term Holding Affects Roll Yield in Commodities

Based solely on time, roll yield will either kill your portfolio as a minor nuisance or accelerate its profits.

Short-Term Positions (Days to Weeks): Trading oil futures or commodity CFDs using a time frame of only two weeks. If your timeframe is two weeks out, then chances are good that you won’t even roll once. Therefore, the effect of roll yield on your return will be less than 1-2%. Your return or loss will depend almost entirely on the movement of the price itself.

Long-Term Positions (Months to Years): Holding that same position for two years will cause roll yield to become the most substantial element. If you had rolled that position 24 times while it remained in a contango situation, with a roll cost of 2% per month, you would have lost approximately 40% of your capital just to market structure alone, even though the spot price was unchanged over that time.

Let’s look at a more specific example to illustrate this point: The VIX futures market is often a prime example of an extremely extreme contango situation. As a result of the fact that traders are paying huge premiums to protect themselves from future volatility, VIX ETFs such as VXX and UVXY are very rarely out of contango.

From 2010 through 2023, VXX has seen a decline in value of being greater than 99% as a result of negative roll yield, and this has occurred regardless of the volatility spikes that occurred during that timeframe. The actual VIX did not lose 99% of its value; it was the VXX that suffered because of the effects of the ETF structure.

On the other hand, throughout the 2007-2008 commodities supercycle, agricultural and energy were two markets that remained in backwardation for long periods of time. Long-term investors in many commodity indices benefited significantly from positive roll yield, either by creating additional positive returns through rolling longer-dated futures contracts, thereby receiving 8-12% more in annual earnings than what they received through put gains based on their current futures contracts.

The benefits of using CFDs or derivative contracts become obvious at that stage. You can have commodity price exposure without needing to roll monthly contracts. You can adjust your position based on the underlying market conditions, and not because of predetermined contract expiration dates.

The example of a monthly crate of apples expands greatly. If you are an individual purchaser, buying just one carton of apples at a slight premium typically doesn't matter. However, when you're a significant supplier purchasing 100 cartons of apples every month for a five-year timeframe in a contango market, those price premiums quickly make a significant difference between profit and loss.

Key takeaway: The longer the investment timeframe, the more important roll yield becomes. What may not matter in the short-term or weeks may become an essential factor in the long-term or months, or severe in the multi-year timeframe.

Contango vs Backwardation Arbitrage: How Institutions Profit and What Retail Investors Should Know

Traders and institutions can make money off contango and backwardation by using arbitrage strategies. Understanding these strategies (and also the limitations to them) provides an understanding of why market structures exist and if they can be the basis for a trading opportunity.

Calendar Spread Arbitrage: This is the most prevalent method of arbitrage, the contango and backwardation. Traders will buy near-month contracts and sell distant month contracts when the futures curve is steep. As the near-month contract approaches expiration, the difference between the two contracts will diminish, and the trader can capitalise on the narrowing of the spread.

In April of 2020, for example, WTI June futures were selling at a premium of $10 over May futures. Traders with sophisticated trading techniques would buy May and sell June, knowing the spread would narrow. As the May contract approached expiration, many traders earned very large profits due to the vast narrowing of the spread. Some traders were earning returns of 50 to 100 per cent on calendar spreads within weeks.

Spot Futures Arbitrage: Also, institutions that possess storage facilities can buy physical commodities in the cash market and sell futures contracts that are in contango. If they have the commodities, they are then able to hold the commodities, capture the contango premium, and then sell the commodities to satisfy the futures contract at expiration.

For example, if an oil trader sees that the spot market is $70 and the futures contract for six months is $78, they buy the physical commodity for $70, store the commodity for $3 per barrel, and sell the futures at $78, solidifying a profit of $5 per barrel. This type of arbitrage transaction is referred to as "cash and carry."

Why Retail Investors Struggle:

The reality is unpleasant. Most of these arbitrage opportunities involve the need for:

-

A significant amount of capital (often in the millions)

-

Access to the areas where you need storage or delivery

-

Low transaction costs (typically paying at an institutional rate)

-

An understanding of the specific contract specifications.

-

The ability to manage margin obligations across multiple positions

Transaction costs often outweigh the potential profits for the average investor; you may find a 3% contango spread, but after paying all commissions, bid-ask spreads, and interest charges, your actual profits may be very close to zero.

CFDs provide a "middle ground". Although you cannot actually perform a physical arbitrage, you can create different types of position structures to benefit from movements in the curve without having to put up the same amount of capital as you would for futures contracts. You also have flexibility in your exposure depending upon market conditions as they change between contango and backwardation.

The most important information to take away from this is that there are arbitrage opportunities available; however, the vast majority of arbitrage opportunities will be taken advantage of by large institutions that have much larger amounts of capital and the necessary infrastructure. Therefore, for retail investors, understanding the structure of these opportunities is more important than the possibility of actually taking advantage of those opportunities for arbitrage.

How to Adjust Your Strategy Based on Contango or Backwardation

It's pointless to understand contango and backwardation if you don't modify your trading strategy accordingly. Here are ideas for matching your approach with the structure of the market.

Trading in Contango Markets:

-

Do not oppose the curve: Contango provides a built-in headwind to long-term buy-and-hold strategies for commodity ETFs. Your options include:

-

Shortening your time horizon: Trade off price movements in a day-to-week timeframe as opposed to months. Get out before the roll yields.

-

Using alternatives to ETFs: Instead of using commodity ETFs, use commodity Contracts for Difference (CFDs) or direct futures, so you can control your roll timing. Staying in the near-month contract allows you to roll only when it is technically advantageous to do so.

-

Using an inverse strategy: In extremely contango situations, the structural decay will allow some traders to profit. This is an advanced strategy that carries a high level of risk; however, taking short positions on certain commodity ETFs can allow you to take advantage of negative roll yield.

-

Concentrate on the momentum: If you want to overcome roll yield drag, you are going to need to see stronger directional moves. A 2% monthly move might not be able to compensate for a 1.5% monthly cost associated with contango.

Trading Backwardation Markets:

A long-term Commodity ETF will do well in Backwardation. In Backwardation, your return will be larger because of the tailwind effect of Backwardation on your positions. Do the following:

-

Increase your holding time: Let the positive Roll Yield Compound. Each time you roll forward, you are getting free returns from the market structure.

-

Increase your position size: The Risk/Reward ratio improves in Backwardation. You will be profiting not only from price appreciation but also from the structural gain.

-

Be alert to shifts in the curve: Backwardation does not last forever. Watch for any signs of the curve flattening or flipping to Contango. A signal that you should either book profits or adjust your position.

-

Take Advantage of the market structure: Many traders actively search out Backwardation markets for their Long-Term trades, knowing the structure is in their favour.

CFD/Derivatives Advantage:

Traditional Exchange Traded Funds (ETFs) have to mechanically roll around a set schedule; however, through the use of Contracts for Difference (CFDs) and direct futures, the trader has more flexibility and control as follows:

-

Staying in the near-month contract if the curves support it.

-

Skipping a month if the roll costs are high.

-

Switching between contract months based on the shape of the curve.

-

Completely avoiding the issue of physical delivery.

Returning to our analogy regarding apples, if the market is in contango (future prices are increasing), the trader may buy only two weeks' worth of apples at one time to limit their risk from increasing costs. Conversely, in the situation of backwardation (future prices decreasing), the trader would lock in supply for a longer-term period at a lower price.

An example of this would be a trader looking at the energy markets in January of 2021 would have seen the change from contango to backwardation take place with the announcement of vaccination deployment; therefore the best strategy would have been to move from focusing on short-term trade tactically to taking a longer-term position and capitalizing on the positive rolling yield during the subsequent rally in oil prices through 2021.

Comparison Table:Key Takeaway: Strategy must align with market structure and holding period. Fighting the curve is expensive. Flowing with it improves your odds dramatically.

Contango, Backwardation, and Roll Yield: Key Takeaways for Smart Commodity Investing

Understanding that price prediction alone will not suffice as an effective investment strategy, and therefore, if you only focus on predicting the price of oil, natural gas or gold and do not take into account how the futures markets operate, then even if your predictions are correct, you will lose money on your investment.

Another area of confusion for investors is the concept of roll yield. Roll yield is a very real component of an investor's return (just as any other component) and can be thought of as the monthly 'leakage' of the investor's returns due to contango, and in contrast, will enhance the investor's returns due to backwardation. Roll yield will often eclipse the impact of actual movements in spot prices over time.

The impact of structure on the outcome of your investment is very real as well. If the price of crude oil increases by 20%, it does not necessarily mean that you will receive a 20% return on your crude oil ETF investment. It may actually be an 8% return due to negative roll yield, or it may be a 25% return due to the benefit of positive roll yield.

To be an effective commodity investor, the following principles should be adhered to:

-

Determine whether contango or backwardation exists before placing a trade.

-

Align the duration of your investment to the current market structure.

-

Utilise investment vehicles that allow for flexibility (i.e. delta one contracts, futures).

-

Continually evaluate the changes in the futures curve, the same way one keeps an eye on market prices.

-

Sometimes the best strategy for an investor is not to invest at all, especially when the futures market structure is significantly against the investor.

Stop letting hidden costs erode your profits. Start trading with structure on your side at BTCDana.com.